Five ways to lower costs and raise staff satisfaction right now

For international schools, health insurance for staff and faculty can seem confusing, difficult to manage and a drain on financial resources even in the best of times. But in the midst of a global pandemic where financial pressures are even more in the forefront and healthcare can often make or break a faculty member’s decisions to return to their existing job or relocate to a new country for a new job, it’s even more important.

As Asia’s most experienced international school health insurance consultants, we hear the same complaints about health insurance all the time: “It’s too complicated.” “Brokers and insurers can’t be trusted.” “Budgeting is impossible, my rates go up every year and I have no idea why.” “It’s a financial black hole.”

Here are five easy wins you can use to break the cycle of yearly health insurance premium increases. Follow these tips to put yourself in the driver’s seat when it comes to managing your school’s group health insurance.

1) Don’t let your insurer decide when you finalize your renewal pricing.

Insurers are often vague when it comes to providing information and data about your plan, and can also be ambiguous when it comes to the methodology that they use to price your plan. This is no accident. Insurers are very careful to try and ensure that they remain in a position of control when it comes to your group health insurance plan.

How many times have you been told that your insurer cannot accurately price your renewal until the last month or two prior to the renewal date? While there is some truth in this if you’ve recently changed insurance providers, if you have been with the same provider for a number of years then the insurer is able to calculate your renewal at any time during the policy year. There’s no reason therefore for you not to be able to do the same.

The key number that insurers will look at when pricing the renewal of a large group plan (those with more than 100 employees) is the claims loss ratio. This is the percentage of total claims versus total premium. Insurance companies will typically look at the last 12 months claims on a rolling basis, regardless of how far into the policy year you might be. Of course it’s reasonable to expect a claims lag time of 2-3 months because hospitals can be slow to submit claims but once you have factored in reasonable lag time, you will then be in a position to review your claims loss ratio at any time, not just towards the end of the policy year.

Track your claims on a monthly basis and you will be in a position to request and/or predict your renewal pricing at any time during the year. If you are not receiving the claims data from your insurer or broker on a monthly basis, make it a requirement going forward. This is even more critical recently as a low level of claims due to the impact of COVID- 19 (with plan members not having elective treatment) and will help with negotiations when it comes time to renew.

2) Reduce premiums without reducing benefits.

With the right information and planning, you can get your health insurance plan into a position where you can expect year-on-year decreases to the premiums.

There are two parts to this. The first part is to ensure that you are getting the right information from your insurer. The second part is to put in place a 1, 3 and 5 year strategy based on what that data tells you.

Some of the key things to look for include whether you have under-utilized benefits. If so, you might consider self-insuring those benefits or removing them from the plan altogether. How many people on your plan are having an annual health check-up? Remember that prevention is better than cure and is much more cost-effective in the long-term. And not only will this increase your staff morale but can help you protect your staff from critical illnesses. Have you done a recent review of your plan’s deductible? If your plan has no deductible, or a low deductible of only US$100, then you might consider increasing the deductible – even a deductible of US$200-300 will be considered by staff to be very reasonable, and will reduce premiums.

Where are your staff going for treatment? If they’re always going to the most expensive clinics and hospitals in your area what can you do to change how they use the plan? You might consider closer partnerships with medical facilities that are not part of your insurer’s high-cost provider list and bring into your workplace doctors from more reasonably-priced facilities for onsite services.

As we have said, the key here is to first ensure that you are getting the right data from your insurer and then, with the help of your insurer or broker, to put in place a 1, 3 and 5 year strategy for plan design adjustments based on what that data tells you. With the right combination of year-on-year plan adjustments, you should start to see a shift in employee claiming practices, and premium savings after just one year.

3) Increase staff satisfaction without paying more by just increasing benefits.

As we’ve just seen, part of the planning for ensuring year-on-year decreases to your group medical insurance premiums includes making plan adjustments. You’re probably thinking that decreasing your staff’s benefits is the fastest way to ensure that you’ll have a line of disgruntled employees lining up outside your office each morning with pitchforks – doesn’t sound like much fun. While any plan design changes need to be handled carefully, with well-planned and early communication with staff regarding the changes, it is our experience that it is possible not only to decrease benefits gradually over the short- to long-term but also to increase staff satisfaction in the plan at the same time.

As part of the communication to staff about why plan design changes are taking place, it’s important to highlight that small plan adjustments are necessary to ensure that as an employer you are able to keep intact the parts of the plan that staff value most in the long-term. These include emergency benefits, hospitalization and cancer treatment.

If you are making plan adjustments that might result in slightly decreased benefits for your staff, there are a number of things you can do for a positive impact on your staff’s lives, such as implementing wellness initiatives or challenges. This can include working in partnership with your insurer or broker to help your staff and their families understand better how to use their plan, bringing GPs or physiotherapists onsite to see your members, or hosting health check-ups onsite at your school or office.

A comprehensive annual health check-up serves as a great early warning mechanism against illnesses and can help find problems before they start, when the costs and chances for treatment and cure are better.

Due to the current pandemic, the last place many people want to be right now is at a hospital. So many private clinics and hospitals are promoting their online or telephone-based medical consultations. Many global insurers, particularly those with specialized international school plans, will include telemedicine as standard.

What’s fantastic about each of these initiatives is that they can often be done free-of-charge without an additional fee and are not part of your insurance premiums. It’s a win-win situation – the school saves money and your staff are happier.

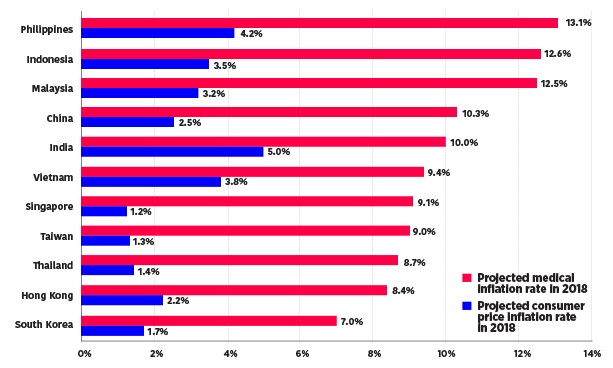

4) Stay ahead of the medical inflation trend.

It might have been previously that you could afford to not take these easy wins and just take the medical inflation trend increase each year. With the financial pressure created by COVID-19 however, now is the time to take action

You’re probably starting to see now how increased transparency on your plan’s claims data, when combined with long-term planning, and wellness and healthcare initiatives outside your normal insurance benefits, puts you in a much stronger position when it comes to managing your health insurance premiums.

Medical inflation in most markets in Asia is generally between 7% and 14%. If you do nothing with your insurance plan – no plan adjustments that might impact how your staff use the plan, have no onsite wellness initiatives, or you do nothing to help your staff live healthier lifestyles then you should correspondingly expect to budget year-on-year increases of between 7 and 14%.

Of course such year-on-year increases are not sustainable. But being in a strong position means being able to budget low, single-digit increases becomes the worst-case scenario.

Even if your plan should experience a catastrophic claim such as cancer cases or a serious accident or long-term illness, your insurer will recognize the long-term planning you have done to keep your claims down. Your insurer will approach your renewal from a position of a partner and therefore not propose a huge spike in premiums, which would mean having to switch providers. We know this to be true because we have experienced such situations with our clients and despite a few high-cost claims over the past few years, we have still seen a general trend of their insurance premiums coming down. Your insurance and your insurance budget need no longer be a black hole.

5) Treat your insurance spend as an investment, not an expense.

We are aware that your health insurance spend can be a significant line item on your school’s finances. This makes it even crazier that so many companies lack transparency and data regarding how their plan is running which makes it so difficult to manage and budget for this expense. The added financial stress of the current COVID environment forces international schools to take a magnifying glass to every expenditure and drive out cost and maximize return at every opportunity – health insurance included.

With the right tools and long-term planning, we hope you will start to see how your company’s insurance spend will no longer be an expense that you cannot control and instead will become an investment in the long-term health and well-being of your staff. You will see an increase in workplace wellness, your staff will better understand their insurance and how to use it, and all of this will become a key driver of employee retention, happiness and well-being.

If you are interested in learning more about how we can help achieve all of this for your company, then get in touch. One World Cover has developed a number of proprietary tools

Need help with your company health insurance or concerned you are overpaying?

One World Cover is an Asia-based insurance consulting company and broker. We consistently help our clients reduce their group health insurance premiums by between 15-30%, without having to make any plan design changes or change insurance provider. Our many international school clients have done this using our proprietary digital Claims Data Analysis Platform (or “Control Room”) which gives our client’s finance team and senior management complete transparency to expose and significantly reduce any excess costs charged by your insurer or current broker. Get in touch: [email protected]